U.S. office demand gained momentum in the second quarter of 2015 as net absorption increased 40 percent year-over-year, according to the latest quarterly U.S. office occupancy report from CBRE.

This further tightened market conditions for renters and pushed second-quarter 2015 downtown (10.6 percent) and suburban (15.1 percent) vacancy toward its previous lows in 2007 of 9.7 percent and 13.9 percent, respectively.

“Market conditions in the U.S. are owner-favorable in most downtown and suburban areas,” reads the report.

Downtown office property is particularly hot, with asking rents surpassing their 2008 peak in the first quarter of 2015 and setting a new historical high of $42.70 in the most recent quarter. Suburban rents increased more slowly and remain 3 percent below 2008 levels.

Click to enlarge

The report also states that San Jose, Seattle, Austin, Orlando, Fort Lauderdale and Phoenix are generating the strongest rates of new demand relative to the size of their respective markets, making conditions more competitive.

The U.S. gross average asking rent increased by 1.1 percent quarter-over-quarter, and by 3.6 percent year-over-year in the second quarter, surpassing its 2008 peak. Double-digit year-over-year rent increases occurred in downtown San Francisco, downtown Manhattan, Seattle, Houston the Boston suburb of Cambridge.

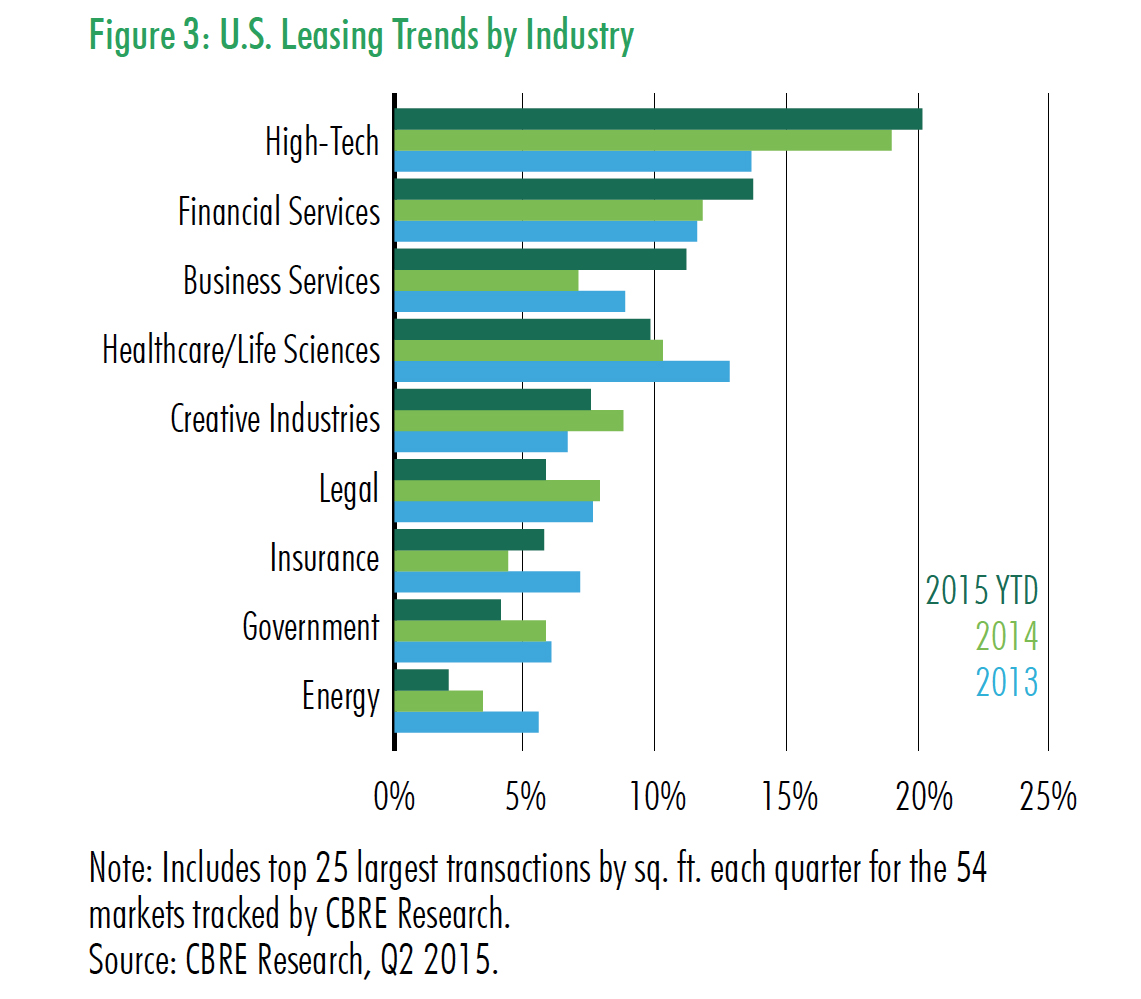

Major leasing activity during the first half of 2015 was dominated by the high-tech sector, accounting for one-fifth of leasing transaction volume. Financial services accounted for the second-largest share, at 13.7 percent, representing an increase over both 2013 and 2014.

“Amid low oil prices and ongoing downsizing in the federal government, the government and energy sectors’ shares of major leasing activity continued to trend down,” reads the report. “Government’s 2013 share of 6 percent had shrunk to 4.1 percent as of the first half of 2015. Energy declined even faster, from 5.5 percent in 2013 to 2.1 percent in the first half of 2015.”

Construction activity has increased, but remains low by historical standards and is concentrated in only a few markets. In the 12-month period ending July 31, quarterly completions averaged 7.3 million square feet, well below the 12-month average of 19 million square feet, which occurred during 2008.

The office market outlook anticipates demand outpacing new supply, resulting in lower vacancy, fewer large blocks of space and higher occupancy costs in the years ahead. Those higher costs will be reflected in rising rents and construction costs for tenant improvements.

Click here to read the full report.

— Haisten Willis