By Jeff Shaw

Freddie Mac and Fannie Mae — collectively known as the government-sponsored enterprises (GSEs) — have been on divergent paths in recent years when it comes to lending in the seniors housing sector. As specifically regards current activity, Freddie Mac is in the midst of a transaction rally, while Fannie Mae is enduring a wave of delinquencies fueled by seniors housing loans.

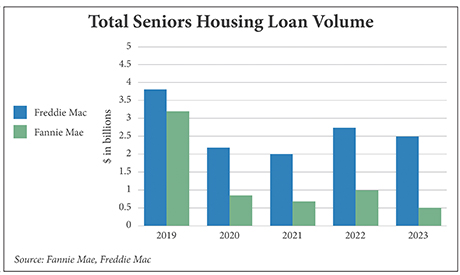

The two lenders posted similar deal volumes in 2019 before the onset of the COVID-19 pandemic, with both closing over $3 billion in loans that year. While loan closings fell during and after that pandemic, the difference in scale of that drop is significant. While Freddie’s annual volume has not fallen below $2 billion, Fannie’s has stayed at or below $1 billion for four years running, and volume fell 50 percent from $1 billion in 2022 to $500 million in 2023.

It’s not hard to see why Fannie Mae is doing less seniors housing business. The organization has a delinquency problem in the sector. Chryssa Halley, Fannie Mae’s CFO, called out the problem on the full-year 2023 financial results conference call.

“Our multifamily serious delinquency rate increased to 46 basis points as of Dec. 31, 2023, from 24 basis points as of the same time the prior year, driven by stress in our seniors housing loans,” she said. “We actively pursue loss mitigation actions when appropriate, such as loan workouts, which may resolve delinquencies. If appropriate workouts cannot be achieved, the loans are foreclosed upon.”

These delinquencies are a noted dark spot on Fannie Mae’s otherwise positive results — net income rose $400 million to $2.6 billion for the organization’s multifamily business in 2023.

As Steve Kennedy, executive managing director at VIUM Capital, put it in a recent Q&A with Seniors Housing Business, “Fannie Mae remains essentially closed for business, and Freddie’s relatively low leverage and reluctance to fund much equity out is not attractive or competitive in many situations.” He went on to call “the reluctance for the GSEs to provide competitive terms” as his biggest surprise over the last year.

For its part, Freddie Mac saw a slight decline in 2023 volume, largely driven by the run-up in interest rates over the last two years. However, Kathy Ryser, Freddie Mac’s multifamily senior director for seniors housing underwriting, is quick to note that other lenders saw an even deeper dip, meaning Freddie “increased market share in 2023.”

Although Freddie’s deal volume has been strong through the first half of 2024, the agency faces the same challenges as the rest of the commercial real estate industry, says Ryser.

“We remain active in seniors housing lending, but 2024 volume will depend on the acquisition activity and refinance opportunities that qualify based on the higher cost of debt,” says Ryser. “Most believe the bid-ask gap in seniors housing property sales is narrowing in comparison to last year, but until long-term interest rates stabilize and cash flows reflect longer stabilization periods, the acquisition market will create limited long-term debt financing opportunities.”

COVID Effects Linger

Ryser says that Freddie Mac’s fundamental business model and underwriting principles “remain the same” compared with prior years, though she acknowledges that the COVID-19 pandemic and the long, slow recovery to pre-pandemic occupancy have skewed the view.

“Over the past few years, the industry has experienced a prolonged pandemic occupancy recovery, reduced operating margins due to inflationary expense pressure and tighter labor markets, as well as reduced sales volume and property values caused by the rapid increase in interest rates,” she says.

“To fulfill our mission of supporting housing for older adults, we consider a range of factors in underwriting. This includes payroll and other variable operating expenses to produce an NOI (net operating income) for loan sizing; alternate exit tests to address the balloon maturity risks; floor capitalization rate for loan sizing at quote; and higher required DCRs [debt coverage ratios] for floating-rate loans based on the max capped note rate.”

By dovetailing seniors housing loans with the agency’s green and affordable programs, Freddie Mac has been able to boost deal volume.

“Loans secured by seniors housing properties qualify for Freddie Mac’s affordable and green programs,” explains Ryser. “Affordable housing is at the core of our mission, and we are in a strong position to help advance that mission.”

Although the future is unclear, with so much depending on the direction of the capital markets, Ryser says that Freddie expects to continue lending in the seniors housing space as much as it can.

“Part of our core principles include working with our established Optigo lender network to partner with borrowers and operators who are financially well positioned and have ample seniors housing experience to care for the older adults in the properties we finance.”