ARLINGTON, VA. — U.S. retail construction activity totaled 64.2 million square feet in the first quarter, down from 70 million square feet in first-quarter 2025 and well below the 10-year average (+90 million square feet), according to research from CoStar Group.

Brandon Svec, national director of retail analytics at CoStar Group, points to multiple governors for new retail construction, including the popularity of e-commerce, competition from other property types and the previous cycles of broad-based expansion in the retail industry. Additionally, he says elevated costs for land, construction materials, labor and debt have made it difficult for retail developers to justify new construction.

“The pullback in construction reflects a development environment that remains difficult to pencil in most markets,” says Svec. “Even in markets with strong population growth and leasing demand, achieving returns that justify ground-up construction has become increasingly challenging.”

Data from the Arlington-based commercial real estate information and analytics firm shows that the nation’s retail development pipeline is sinking to levels not seen since the previous two cyclical lows: the early stages of the COVID-19 recovery and coming out of the Great Financial Crisis in 2011.

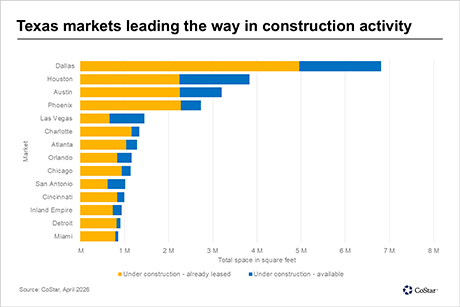

Among markets tracked by CoStar, three Texas markets are leading the way in terms of new construction: Dallas, Houston and Austin. These markets are the only ones that have pipelines above 3 million square feet.

The top 10 markets for first-quarter retail construction activity are:

- Dallas

- Houston

- Austin

- Phoenix

- Las Vegas

- Charlotte

- Atlanta

- Orlando

- Chicago

- San Antonio

CoStar reports that in the top Texas markets, as well as their counterparts in the Southeast and Southwest, the retail space in the pipeline is mostly preleased. On the flip side, most markets in the Midwest, West Coast and Northeast have fewer than 1 million square feet underway and higher concentrations of unleased space, according to CoStar.

— Staff Reports