CHICAGO — After years of uncertainty fueled by inflation, rising interest rates and changing consumer behavior, retail real estate has entered a notably different phase. According to JLL’s 2026 U.S. Retail Thematic Outlook and Investor Survey, the sector is no longer in recovery mode — it’s operating from a position of strength.

Retail activity surged in the first quarter of the year as transaction volume hit $13.5 billion, a 5 percent year-over-year increase. Concurrently, the trailing 12-month volume climbed to $62 billion, representing a 31 percent increase over the previous period. Retail now accounts for its highest share of U.S. sector investment in a decade, sitting at 14 percent.

The survey of nearly 150 retail investors paints a picture of a market supported by historically limited new supply, healthy consumer demand and renewed investor confidence. While broader economic concerns remain, the outlook suggests retail has become one of commercial real estate’s most compelling investment narratives, driven by strong fundamentals.

One of the clearest indicators of that confidence is investor appetite. Nearly two-thirds (64 percent) of respondents said they expect to increase retail acquisitions in 2026, while fewer than half (48 percent) anticipate selling more assets.

The imbalance between buyers and sellers is creating an increasingly competitive investment environment, with demand for quality retail properties continuing to outpace available inventory. More than half of investors also believe the retail market has entered a “mid-cycle” phase, where occupancy, rent growth and property performance remain healthy.

In addition, development has remained muted for several years due to elevated construction costs and financing challenges, leaving little new inventory to enter the market. Net retail deliveries in first-quarter 2026 totaled 7.8 million square feet, which is 25 percent below the decade’s quarterly average, according to JLL research.

With this outcome, existing shopping centers have benefitted from low vacancy rates and increased landlord pricing power. Owners are seeing stronger leasing activity with the ability to push rents higher as retailers compete for quality space. These dynamics have become one of the defining characteristics of today’s retail market.

Investment Categories

More than 80 percent of investors continue to target grocery-anchored assets, reflecting the stability provided by necessity-based shopping and consistent consumer traffic. While grocery-anchored shopping centers remain the industry’s gold standard, the survey highlights growing enthusiasm for another property type: power centers.

Nearly three-quarters of respondents are also actively pursuing power centers, illustrating the market’s increasing confidence in large-format retail that is anchored by service-oriented and category-leading tenants. The narrowing gap in pricing between grocery-anchored and power centers reflects how investors increasingly view both formats as dependable and resilient.

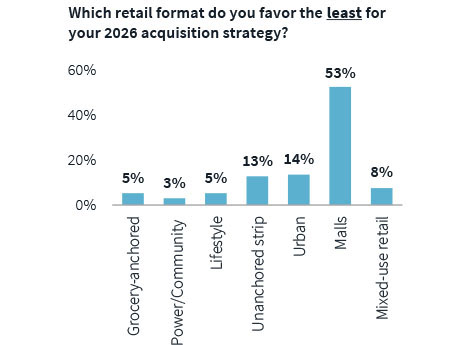

While grocery-anchored (39 percent) and power centers (32 percent) are considered the most favorable retail format for investor acquisition strategy, malls are favored the least by more than 50 percent of investors — a drastic change from previous years.

The emphasis on necessity-based retail reveals the overwhelming concentration of investor interest around grocery and discount retailers. Grocery retailers command 38 percent of all investor commentary, followed by discount department stores at 18 percent, apparel at 11 percent and quick-service restaurants (QSR) at 9 percent. These retail formats remain among the most sought-after properties, reflecting a broader shift toward retailers that deliver everyday value as consumers continue balancing inflationary pressures with household budgets.

In addition, investors often chose Whole Foods Market as their top tenant choice (59 percent), followed by TJX Brands (56 percent), Trader Joe’s (41 percent), Target (23 percent) and lululemon (18 percent).

Another notable trend emerging from the survey is investors’ growing willingness to pursue opportunities beyond the nation’s largest metropolitan areas. Approximately 68 percent of respondents indicated they would rather seek higher returns in secondary and tertiary markets than compete for more expensive assets in primary markets.

Optimistic but Cautious

Despite the optimism, investors have not abandoned a cautious mindset. Economic slowdown and geopolitical uncertainty now rank among the industry’s primary concerns, replacing previous financing challenges as new development remains stymied.

Although newly built retail centers can demand premium rents, escalating construction costs continue to make many projects financially difficult to justify, limiting future supply and reinforcing the competitive advantages utilized by existing retail properties.

While JLL’s outlook points to a retail sector that has emerged as one of commercial real estate’s strongest-performing asset classes, familiar factors are still igniting a competitive environment for quality retail properties.

JLL’s 2026 Retail Investor Survey captures insights from nearly 150 investors across the United States. Survey data reflects current investor sentiment and strategic positioning within the retail real estate market as of first-half 2026, with a forward-looking view over the next 12 months. Survey participants included institutional investors, private investors, public investors and other investment entities.

— Abby Cox