By Taylor Williams

The roller coaster ride continues.

That’s more or less the joint takeaway from Northeast Real Estate Business’ annual reader forecast surveys for commercial brokers and developers/owners. For if the past 12 months have revealed anything about the economic and geopolitical factors that impact deal volume, investor sentiment and overall industry health, it’s that those dynamics are wildly unpredictable and highly subject to change.

In last year’s survey, respondents across both groups expressed optimism — albeit guarded — for better business prospects in 2025. The incoming Trump administration was viewed as pro-business, and the previous year had ended with a trio of long-awaited cuts to short-term interest rates. Capital sources on both the debt and equity sides of the market envisioned a new, more prosperous chapter in 2025 as 2024 closed with subsided inflation, healthy job growth and less volatility in the 10-year Treasury yield.

Editor’s note: In mid-November, Northeast Real Estate Business sent email invitations to participate in the annual online survey to three separate groups — brokers; developers, owners and managers; and lenders and financial intermediaries. The survey was held open through mid-December. Invitations to participate were also included in the Northeast Real Estate Business e-newsletter, as well as through ReBusinessOnline.com.

Although fundamentals had undoubtedly softened in two key asset classes — multifamily and industrial — that could be chalked up to cyclical ebbs and flows, and shifting macroeconomic conditions should usher in a rebound across commercial real estate as a whole. Or so the expectations went.

It would take only a couple months for that script to be drastically rewritten. As the Trump administration moved rapidly and aggressively to trim the federal workforce, establish new tariff policies and lay the groundwork for fresh tax-cut-based legislation, the business community found itself awash in unexpected uncertainty.

By late summer, the U.S. economic foundation appeared to have settled, giving commercial real estate professionals optimism for a strong fourth quarter. But those hopes too would be dashed by the politicizing of the Bureau of Labor Statistics, which produces the monthly jobs report, backlash to the

AI-driven data center boom and the longest government shutdown in recent history.

“Uncertainty makes this a challenging deal environment,” observed survey participant Sam Obar, president and principal at regional brokerage firm Obar Property Group. “There is a general feeling that the economy is trending downward, but loans are still generally available and unemployment is still manageable. That unpredictability makes it hard to value properties, although this appears to be nothing new, as we were facing much of the same challenge in the beginning of 2025.”

Is it any wonder, therefore, that commercial real estate professionals are reluctant to make bold predictions for 2026? Or that among those predictions that are made, discrepancies and inconsistencies abound? Such was the case when assessing the results of our surveys for Northeast brokers and developers, which are similar but not identical.

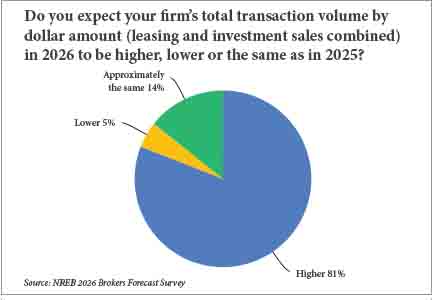

For example, among brokers, 81 percent of respondents believed that their firms’ total transaction volume by dollar amount, inclusive of both leasing and investment sales, would be higher in 2026 than 2025 (see chart below).

That finding is not especially surprising at all for a group that is renown for its eternal optimism. Yet within that 81 percent of respondents, the expected magnitude of the increase was anything but uniform. About 35 percent of those respondents said they expected their deal volume to grow by 5 to 10 percent, while another 30 percent projected year-over-year growth in excess of 20 percent. Another 30 percent pegged 11 to 15 percent as the anticipated annual rate of growth.

Developers/owners were equally split in terms of whether they expected to be net buyers or sellers in 2026. Of the total respondent pool, 33 percent said net buyers, 17 percent said net sellers and 41 percent selected the “uncertain” option — the final choice attesting to the underlying mindset in the marketplace as a whole.

This group was also divided with regard to confidence that their development pipelines would expand in 2026 relative to 2025, although the majority (33 percent) expressed “high confidence” that such a scenario would come to fruition.

Rate Expectations

As a group, however, developers were more aligned in their belief that borrowing costs would not be worse in 2026. Among those surveyed, 67 percent said that the lending climate for new development would either be better or about the same as 2025; the same view and percentage prevailed in terms of the lending climate for acquisitions and refinancings.

And that would seemingly be good news, not just for obvious reasons, but also because 68 percent of developer respondents also cited interest rates as the single-biggest factor that would impact the industry in 2026. That finding could, however, be residual in nature, as owners have spent the better part of the past three years fixated on interest rate movement.

But again, given the events of the past 12 months, it bears repeating that this is all pure conjecture. And while debt may further loosen in 2026, there is no guarantee that equity sources, which have come to represent key absences in capital stacks over the past couple years, will meaningfully follow suit.

“The greatest challenge for the commercial real estate industry remains that capital is tight across the board. Equity is harder to raise and investors are cautious to come to the table after several years of repricing and underperformance,” noted Jon Beaulieu, co-founder of Millstone Property Management, a full-service firm based in Philadelphia.

“While debt is available, underwriting has become much more disciplined. Though deals are still getting done, it’s less frequent and only when assets have extremely solid fundamentals,” Beaulieu wrote. “To add to all this, the industry is expectantly waiting for a meaningful wall of loan maturities to come through in 2027. That refinancing risk will continue to put pressure on pricing and slow transaction activity where values and expectations don’t quite line up.”

Brokers, on the other hand, were more pointed in their assessment of the debt market. Of those that responded, a total of 94 percent stated that interest rates would either decrease (71 percent) or remain the same (23 percent) in 2026 compared to 2025. About 61 percent of brokers also pegged interest rates as the most important determinant of industry health and activity in the new year.

Within both groups of participants, about 30 percent declined to speculate on where the 10-year Treasury yield would likely land in 12 months’ time. Brokers vacillated considerably on this query, with respondents selecting answers as low as 2.5 percent and as high as 5.5 percent. Developers seemed to predict more stability in the benchmark rate, with all respondents who speculated on the metric selecting a final 2026 yield of somewhere between 3.5 and 4.5 percent.

Hope for Office?

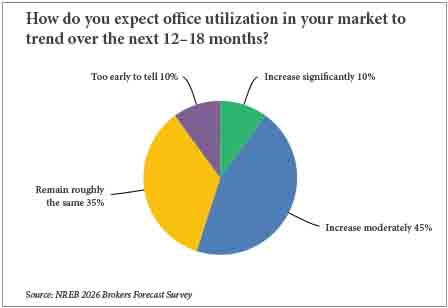

The only other area in which brokers and developers seemed to be in agreement involved, strangely enough, office utilization.

Within both groups, between 75 and 80 percent of respondents stated that they expected rates of office utilization to either remain the same or increase moderately in 2026 as major employers across multiple industries continue to adjust the remote and hybrid work schedules (see chart below).

The sector as a whole remains embattled, although select submarkets have seen occupancy rebounds in the past 18 to 24 months, with Class A trophy buildings tending to emerge as clear winners.

“We are extremely bullish on trophy, Class A office product heading into 2026,” wrote Edwin Cohen, principal at New Jersey-based developer Prism Capital Partners. “Today, ‘Class A’ has a different connotation and is tied to more than just the beautification of a building and how great it looks from the street. It’s where can you walk to, the lifestyle amenities integrated within the building and the immediate surroundings.”

“We truly believe the old adage ‘location, location, location’ is more relevant than ever,” he continued. “Properties that deliver the whole package will perform very well in both the short and long term.” That said, this is not an environment of ‘easy’ dealmaking. Every transaction has its own nuances, yet across the board they mandate a flexible, market-reactive approach. The key to success as an owner today — beyond offering top-level, high-demand product — is staying power, which requires deep resources and good partners.”

— This article first appeared in the January/February 2026 issue of Northeast Real Estate Business magazine.