By Taylor Williams

ATLANTA — Depending on the era in which you came of age and the general experiences you’ve had in life, the notion that “things can always get worse” can be easy to endorse.

As it pertains to commercial lending and borrowing, the consensus narratives that have prevailed ever since the Federal Reserve began jacking up interest rates in early 2022 have largely followed the same script:

“Hunker down.”

“Survive till ’25.”

“Delay and defer.”

In other words, do whatever you have to do to avoid the sting of the 11 interest rate hikes totaling 500-plus basis points that have been enacted over the past 20 months, raising the federal funds rate from near zero percent to its current target range of 5.25 to 5.5 percent.

According to data compiled by Walker & Dunlop, the average all-in interest rate on a 10-year, fixed-rate Fannie Mae mortgage — assuming a conservative structure of 55 percent loan-to-value — is roughly 6.25 percent.

Since rate hikes began, multifamily lenders across various markets have stated that leverage ratios in the neighborhood of 55 to 60 percent have become the norm, all other factors being held equal.

Cloud of Uncertainty

Despite some seemingly telling signals from the nation’s central bank at times, the simple fact is that no lender or borrower really knows for certain just how deep into the cycle of rate hikes the U.S. economy is exactly. If you accept that premise at face value, then you can just as easily argue that now, not next year, is the more sensible time for multifamily borrowers to address impending loan maturities.

Such was the consensus among a panel of commercial lenders who gathered at the annual InterFace Multifamily Southeast conference, which took place Thursday, Nov. 30 at the Westin Buckhead hotel in Atlanta. More than 300 developers, operators and capital markets professionals attended the event, now in its 14th year of running. Hagan Dick, executive vice president and principal at Colliers’ Atlanta office, moderated the discussion.

“I personally think that there are rough times ahead and don’t believe that rates will be much lower at this time next year than they are today, particularly with the drop in Treasuries that we’ve seen over the last 30 days,” said panelist Jason Scott, managing director and head of conventional loan production at Regions Bank. “So, if you have a debt offering in front of you that works today, you should take it.”

“If you’re facing an [impending loan] maturity, the worst thing you can do to yourself and your property is wait and bet on something that may or may not happen by the time your balloon [payment] comes due,” added panelist Chad Hagwood, senior managing director and regional director at Lument, a New York City-based direct lender. “At a bare minimum, you have to see where you are today and decide whether to roll the dice or keep the bird in hand.”

The panelists, all of whom made clear to the audience that they were open for business, would eventually cite several lines of reasoning in formulating their arguments. But while the question of whether or not to pull the trigger on a refinancing can — and will be — dissected through a variety of complex economic and geopolitical lenses, the decision ultimately hinges on what lenders and borrowers think the Fed will do.

In the absence of a crystal ball, lenders rely on a blend of experience and intuition to advise clients on how to navigate interest rate hikes. If their analysis and gut instinct tell them that no major rate cuts are forthcoming anytime soon, then advising their clients to refinance now is simply acting within their fiduciary obligations.

Hagwood added that this line of thinking has helped Lument continue to close a deal per week on average in 2023. Specifically for owners that plan to hold their properties for the long haul but are still facing near-term capital calls, there’s safety in taking money at today’s known price points.

Otherwise, owners risk having to refinance at potentially higher rates in 2024 or 2025. “Yesterday was the time to start looking if you have a maturity in the next 12 to 24 months,” emphasized Hagwood.

Why Now?

Citing uncertainties surrounding the future direction of the 10-year Treasury yield and the outcome of the 2024 U.S. presidential election, the panelists put forth compelling arguments on why it could well make sense to transact now.

For starters, financial markets of all types have historically shown greater volatility in the run-up to presidential elections. Hiking — or cutting — rates by a significant amount over the next 12 months would likely roil markets further and cause major swings. Panelist Jeff Klar, vice president at Miami-based commercial finance firm Bayview Asset Management, suggested that for this reason, political influence would not likely factor into the Fed’s decision-making process.

“With next year being an election year, we expect interest rate [movement] to remain pretty stagnant,” said Klar. “The folks waiting for rates to decrease might not want to get their near-term hopes up because neither [political] side will want to rattle the cages in their pitch to get elected or re-elected. So, if you have a good opportunity, definitely consider it.”

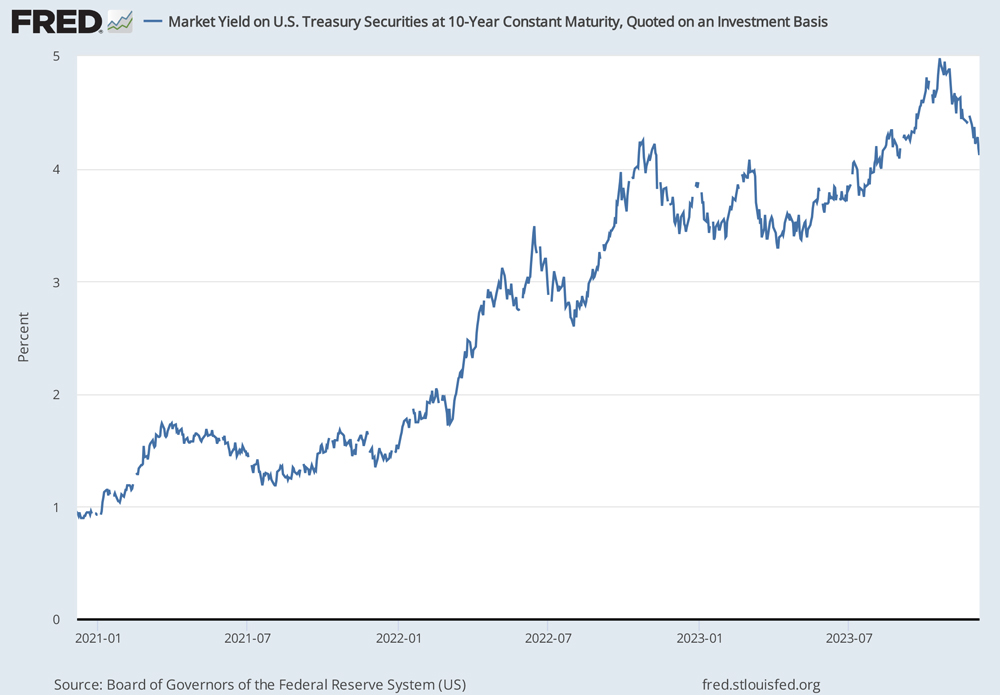

The U.S. 10-year Treasury yield is considered the benchmark against which alternative, riskier investments like real estate are evaluated. Yields on these notes soared over an approximate 18-month period as inflation raged throughout the economy but are now compressing due to lower demand from both U.S. and foreign investors (and governments).

The U.S. 10-year yield closed at 4.13 percent on Thursday, Dec. 7, down from the 2023 high of 4.9 percent in mid-October, but still up nearly 100 basis points on a year-over-year basis.

Other Arguments

Some arguments were simpler and predicated on supply and demand.

Prior to the Fed kickstarting its war on inflation by raising rates, multifamily owners in major markets had been the beneficiary of some record rent growth. And although today’s higher interest rates should choke multifamily supply growth in the future, thus keeping rents high, developers maximized their output when rates were low.

With many of those projects now coming on line, rent growth could remain muted in the short run, thus encouraging borrowers to refinance now rather than face the double whammy of declining rents and rising costs of debt in the near future.

“Fundamentals are a little bit of a headwind right now because we have a major wave of new supply coming,” summarized panelist Henry Lange, regional director at Northwestern Mutual Real Estate. “But you can still take a long-term perspective, look at the basis at which you can get in today and find some attractive opportunities.”

Other panelists pointed out that more job losses could be forthcoming in 2024. Lower levels of employment translate to aggregately less disposable income for rent, adversely affecting owners’ ability to push rents and maximize cash flows of multifamily properties. Such a scenario would augment the upward pressure on cap rates that has already taken place due to interest rate hikes.

Unsurprisingly, inflation factored into the panel discussion. While the average cost of goods and services has decreased in response to rate hikes, getting the rate inside the Fed’s target goal of 2 percent has proven difficult in recent months. For lenders and investors who believe this pattern will hold, refinancing now makes sense. Panelist Ryan Simonetti, co-founder and chairman of New York City-based intermediary Ease Capital, laid out such a scenario.

“The inflation in the United States and Western countries is structural,” he said. “There is an unwinding of the global supply chain that is happening in real time. That’s going to keep costs up — period, full stop. This is the largest [period] of fiscal spending in decades; we have a [$1 trillion] infrastructure act, and that money hasn’t even started to hit the system. We have major projects like a semiconductor manufacturing plant outside of Syracuse — the largest investment in the history of New York State — and we don’t have the people to build it or the people to work it. That will bring wages up.”

Circling back to the subject of Treasuries, Simonetti noted that the two largest buyers of these notes — the U.S. and Chinese governments — are scaling back purchases. When the Fed needs to lower the money supply or deflate the economy, it sells Treasuries. That’s now a tougher sell — no pun intended.

Investors that take these trends as gospel and believe in the staying power of inflation should therefore be inspired to transact now, the panelists concluded.

Following this analysis on Treasuries was a brief aside on the subject of national debt, which is now approaching $34 trillion. When the government operates at a budget deficit, as is the case now, the Fed looks to sell Treasuries to raise revenue and cut into the deficit. These new bonds are being issued and sold to check the growing national debt at a time in which demand for Treasuries is waning. Meanwhile, the government is paying higher yields to existing bondholders whose notes are maturing.

All of that to say that in times of high economic turbulence, sometimes a little unconventional thinking can go a long way.